With mutual fund and ETF fees continuing to fall (and zero fee funds now available), the spotlight is shifting towards financial advisor compensation.

Tim Buckley, CEO of Vanguard presented to 250 Vanguard investors last night. I was there. One of his big initiative is to democratizing financial advice by driving adviser fees “to index fund levels.”

Fasten your seatbelts, folks. Change is coming.

— Rick Ferri, CFA (@Rick_Ferri) October 5, 2018

One of the biggest stories in investing over the past ten years has been a shift away from expensive, actively managed mutual funds towards lower cost, index-based mutual funds and ETFs. Coinciding with this trend has been the rise of fee-based registered investment advisors (RIAs) and the decline of commission-based brokers. RIAs are paid a percentage of client assets (for example, RIAs might charge 1% of client assets annually for ongoing advice; $100,000 account = $1,000 in advisor fees each year). In contrast, brokers receive commissions based on investments they sell (for example, a one-time 5% commission; $5,000 on a $100,000 investment).

Besides the fee structure, the key difference is that fee-based advisors have a fiduciary obligation, where they are legally required to put clients’ best interests ahead of their own. Brokers operate under a suitability requirement, a lower standard which introduces the potential for conflicts of interest. The simplest way to think about this is to consider a scenario where a broker presents two investment options to a client, both of which are suitable. Option 1 is best for the client, but pays the broker a smaller commission. Option 2 is still suitable for the client and pays the broker a higher commission. Whereas the investment advisor must select the best option for the client’s financial future, the broker can select the best option for their own financial future. Brokers might also be tempted to unnecessarily churn client accounts, buying and selling investments to generate additional commissions. If you want a quick, colorful portrayal of the difference between a fiduciary advisor and a broker, here’s one of my favorites:

Under the broker model, opaqueness is the name of the game as “financial advice” fees/commissions are embedded in the broker’s recommended investments. On the other hand, with fee-based advisors, transparency rules the day, with financial advice fees separated from any suggested investments. However, with greater transparency comes additional scrutiny, which brings us to Tim Buckley’s comments. While there have been rumblings over advisor fees since the proliferation of low cost “robo-advisors”, the conversation is picking up steam.

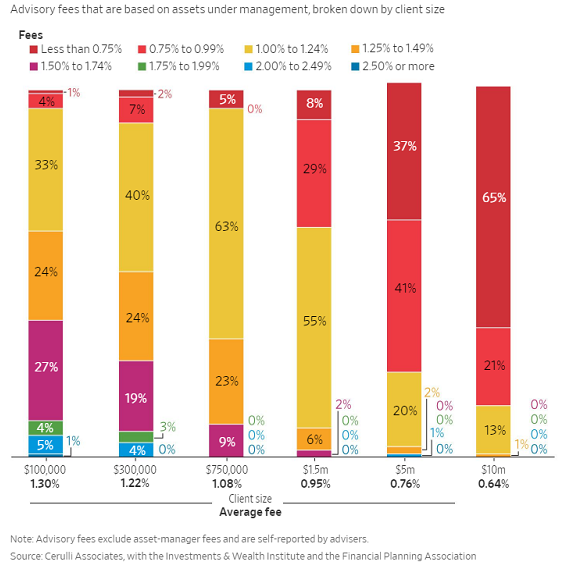

According to a recent Wall Street Journal article, the majority of investors with $1.5 million or less pay fee-based advisors between 1% and 1.5% of their assets under management (AUM) annually.

To further illustrate, a $300,000 account at a 1.22% fee would equal $3,660 in fees annually. For a $1.5 million account, a 0.95% fee would equate to $14,250 each year. Two questions are being raised: 1) Is this fair compensation? 2) Should higher dollar clients pay more in financial advice fees?

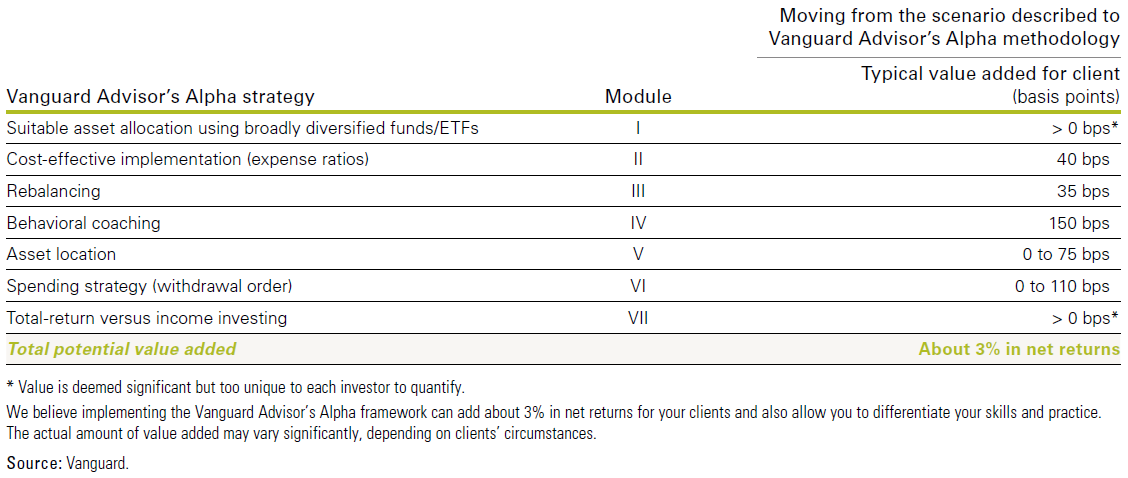

As it relates to the first question, Vanguard themselves found high-quality advisors have the potential to add about 3% annually through things like selecting cost-effective investments, disciplined rebalancing, behavioral coaching, and ensuring investments are located in proper accounts.

The single biggest value-add advisors can bring to the table is behavioral coaching. Poor investment behaviors – bailing on an investment plan at exactly the wrong time, going all-in on that hot tech stock at the top, reacting to talking heads on CNBC – result in the average investor underperforming over time.

Source: JP Morgan

Source: JP Morgan

Source:

Source:

While numbers surrounding investor behavior get squishy and can certainly be debated, for argument’s sake, let’s assume a good advisor can add 1.5% annually simply by ensuring clients stay on track behaviorally. For a $300,000 account, that equates to $4,500 in annual value and for a $1.5 million account, $22,500. In both cases, the advisor’s value exceeds their fees and, again, we’re only talking about the investment side of the equation. As part of their % AUM fee, a quality advisor should also be providing value via comprehensive financial planning – everything from budgeting to retirement forecasting to coordinating estate planning issues. So, is 1% of AUM fair compensation? I think it depends on the investor. If an investor is prone to emotional decisions (and assuming the advisor is not), then an advisor is worth their weight in gold. Ritholtz’s Josh Brown explains this well:

“A true financial advisor doesn’t really earn their fees until the big moment. That moment where a client wants to double their exposure to technology stocks after a 500% rally they feel they didn’t get enough out of. That moment where someone with a thirty year retirement ahead of them is about to succumb to volatility and liquidate a stock portfolio after 8 months of a bear market. That moment where a client wants to shift to an all US stock portfolio precisely as international stocks are on the verge of going on a five year stretch of massive outperformance. That moment when a client is tempted to put five percent of their net worth into Bitcoin at $18,000 per…whatever, coin I guess? And when these moments happen, the advice they get at that time is not simply worth a basis point fee. It’s worth everything.”

And, remember, a true advisor should not only coach good investment behavior, but also ensure the use of low-cost investments, conduct disciplined portfolio rebalancing, locate assets in the right places, and more. Now, could investors receive some of this advice at “index funds levels” through another avenue, perhaps a robo-advisor or call center advisor? Sure. Again, it depends on what you need. If you’re looking for basic asset allocation and rebalancing, a robo-advisor is great. If you’re comfortable talking to someone via phone or Skype, a call center advisor can work just fine. Some call center advisors are even staffed with Certified Financial Planners, providing advice beyond investments. You just have to be comfortable spilling the details of your financial life over the phone.

For other investors, the experience of investing is simply too personal and emotional. When the market is down 15%, waiting in a phone queue or trying to login to an overloaded website isn’t enough. They want to talk to someone. They want to look an advisor in the eyes. They want to sit down face-to-face with the person they’ve developed trust with over the years. Outside of family and health, money might be the most intimate, personal area of someone’s life. Furthermore, a personal relationship with an advisor is usually much more than just investments or a financial plan. Many advisors attend clients’ weddings, funerals, and birthday celebrations. They see clients in the community – at soccer games, the grocery store, the coffee shop. Some advisors may even help clients’ businesses, providing referrals or connecting them with prospective employees. There’s a level of intimacy to this type of relationship, which helps provide context for a client’s overall financial life. Is filling out an impersonal risk assessment with no conversation to provide context and then getting plugged into a cookie-cutter portfolio enough for investors? For some, it’s perfectly fine. For many others, it’s not enough. Ultimately, the question is not what you are paying, but the value you are receiving. The level of service required and the perceived value of those services will vary from person to person. The best option is the one that works for you.

Loved the insights from @nategeraci on changing advisory landscape and robo-advisors: http://t.co/wcVHhvMdS5 pic.twitter.com/VdaCwlldpo

— Michael Johnston (@mjohnsto) May 26, 2015

So, is advisor compensation fair overall? Most advisors I know make an honest living, no different than any other professional service provider. Investment advisors are often compared to doctors, dentists, and lawyers. As it turns out, advisors are the lowest paid of the bunch. Ultimately, the market sets the appropriate wages for any profession.

As it pertains to the second question, “Should higher dollar clients pay more in financial advice fees?”, the answer is more nuanced. Going back to the assumption that a good advisor can potentially add 1.5% in value annually, it’s helpful to sort of invert this question to something like, “Should a $1.5 million investor receiving $22,500 in value pay the same as a $300,000 investor receiving $4,500 in value?”. Different people will have different perspectives. Higher net worth clients do tend to have more complex financial situations and are, therefore, costlier to serve. That said, most advisors acknowledge that costs don’t increase dollar-for-dollar and so they offer tiered fee schedules, with fees declining the greater the client assets. Besides the absolute dollar value a good advisor can provide, perhaps the biggest argument for higher dollar clients paying more in advisory fees is the liability assumed by the advisor. You better believe every client holds their advisor responsible for their investments. An advisor has more risk on the line managing a $1.5 million account versus a $300,000 account.

An alternative to the fee-based model is a flat fee or retainer. Under this arrangement, a client might pay $5,000/year, regardless of the value of their account. For the $1.5 million investor, this might be a great deal. For a $300,000 investor, not so much. The problem with flat fee models is they tend to ignore the smaller dollar clients, whereas a fee-based model can service them well. Are higher dollar clients subsidizing lower dollar clients under the fee-based model? Probably, to a certain degree. Is that bad? Again, subject to debate. Should lower value accounts have access to high quality financial advice? If so, how should that business model look if not fee-based? Healthy people subsidize unhealthy people in the world of health insurance.

More relevant to the financial advisory world, remember – in a fee-based arrangement, the advisor has skin in the game. Interests are directly aligned. If an account goes up in value, the advisor gets a pay raise. If the account goes down, the advisor gets a pay cut. Will an advisor providing a flat fee arrangement feel as incentivized to eat, sleep, and breathe their clients’ investments? Again, subject to debate.

Also, is the flat fee model sustainable from a business perspective? There’s probably a sweet spot in the market for this pricing structure, but the jury’s still out on whether it can thrive at a higher scale. Can flat fee advisors provide the absolute highest level of financial planning at their rate? Perhaps, but you only have to look to robo-advisors to see that rock bottom advisory fees aren’t always maintainable. Earlier this year, Wealthfront – one of the largest robo-advisors, began defaulting clients into a proprietary, higher cost risk parity fund. Why? Because, like any business, there’s a cost to providing services. Maybe they’re not charging enough for advice to operate a sustainable business model, so they need to make money elsewhere. Even for a firm like Vanguard, the question has to be asked whether their low cost financial advice service is operating as a true fiduciary when they route clients solely into Vanguard funds. While investors could certainly do much worse than being invested in Vanguard funds, is this truly independent, conflict-free advice? Is Vanguard subsidizing low cost advice through their investment funds? It’s easy to charge “index fund levels” for advice if you’re making money elsewhere.

There are lots of questions on the topic of advisor compensation and no clear-cut answers. As it relates to the flat fee model, should we apply this same logic across the entire asset management industry? Should an investor plunking $1.5 million into Vanguard’s Wellington Fund pay the same as an investor putting $300,000 to work? Is this a model asset managers will embrace? Seems unlikely. Some argue that charging a % AUM fee places too much focus on the investment component and not enough on other aspects of a client’s financial life. But isn’t a good investment plan and a healthy nest egg central to everyone’s longer-term financial independence?

In the end, I think it’s constructive that advisor fees are being examined. I do think some fee compression is inevitable. However, like doctors, dentists, and lawyers, the market will find the proper clearing rate for services rendered. For advisors not adding value outside of basic portfolio construction, robo advisors are a real threat. Earlier this year, I attended an ETF conference where Vanguard’s Tim Buckley actually delivered the opening keynote address. He presented data showing 58% of advisors are susceptible to losing their jobs to automation and said he expected downward pressure on fees. However, Buckley also said forward-thinking advisors will leverage technology to free-up time to focus on more value-added activities for their clients – things like managing behavior and developing custom solutions. Ultimately, investors will determine whether the value from the advice they receive is commensurate with the fees they are paying. Advisors must justify their value proposition. I’ll leave you with this from the aforementioned Josh Brown after last week’s market action:

You know what kind of conversations advisors are not having with clients this week? Basis point fees.

— Downtown Josh Brown (@ReformedBroker) October 11, 2018