I’m not the guy waiting in line at the Apple store for the latest iPhone release. I let millions of other people roll the dice on Uber and Airbnb before I made the leap. I’m just not an “early adopter”, it’s not in my DNA. I’m much more of a risk manager. However, when it came to ETFs, something compelled me to make the early leap. Fine, I’ll self-proclaim myself an ETF “innovator”. Why bring this up? The Investment Company Institute (ICI) recently released their 2018 Fact Book, a treasure trove of data and charts on trends in mutual funds and ETFs. Among the wealth of information, this happened to catch my attention:

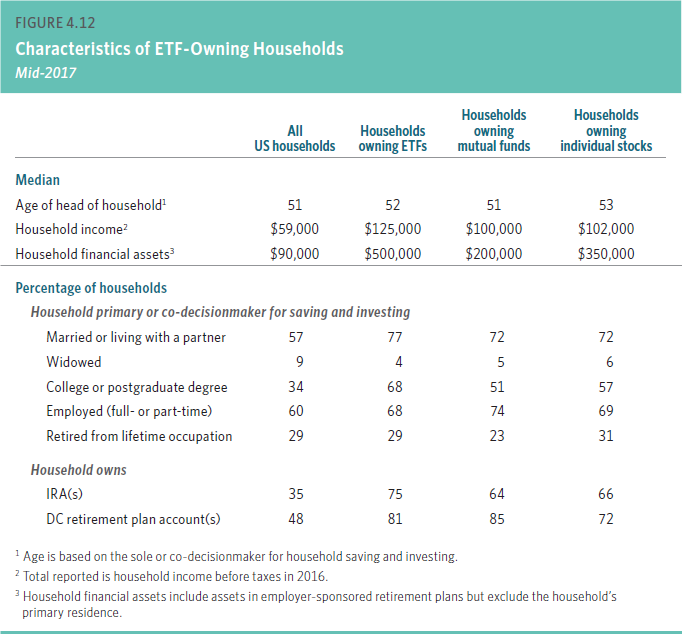

Note that households owning ETFs tend to have higher incomes, greater financial assets, and more education than households owning mutual funds or individual stocks. ETF investors are also more likely to be married or living with a partner and own an individual retirement account (IRA). You can torture data to make it say whatever you want, but the differences – in financial assets and education, in particular – are noteworthy. Median household financial assets (excluding primary residence) for ETF owners are $500,000 compared to $200,000 for mutual fund owners. 68% of ETF owners have a college or postgraduate degree compared to 51% for mutual funds. The bottom line is ETF investors have more assets and education.

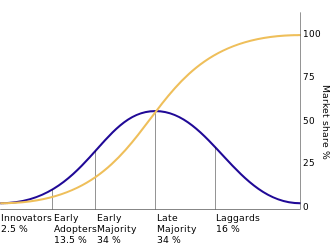

ETFs are often compared to new, disruptive technologies. New technologies are typically adopted over a period of time. In the book Diffusion of Innovations, Professor Everett Rogers suggested technology adoption can be broken down into five categories:

The basic idea is that innovators take the initial risk of exploring a new technology (i.e. spending time, money, and potentially social capital to see if a new idea works – think Betamax versus VHS or more recently, hotels vs Airbnb). If a technology has merit, early adopters move in, followed by the early majority. Once the average person has bought in, then the late majority and laggards finally capitulate and join the crowd. Think about any relatively new technology – from Netflix to Uber to Twitter. You can imagine how a few people initially took the plunge and gave these services a try. Clearly, enough people had positive experiences to generate word of mouth buzz which convinced early adopters to give it a whirl. The technologies spread from there.

It’s my belief we are still in the early stages of ETF adoption. If I had to speculate, I’d say we’re somewhere between the “early adopters” and “early majority” phase. If you think that sounds unreasonable given the significant ETF growth we’ve already experienced, consider that ETFs currently own only 6% of the entire U.S. stock market.

The ICI data now begins to make sense. This from Wikipedia:

“Early adopters have a higher social status, financial liquidity, advanced education and are more socially forward than late adopters.”

Look, there may be other valid reasons why ETF owners tend to have higher incomes, greater financial assets, and more education. And, there are plenty of non-ETF owners with significantly higher salaries, assets, and levels of schooling than some ETF owners. Clearly, buying ETFs doesn’t come with an MBA and salary increase.

But… early technology adopters and early ETF investors share many similar characteristics. Most people I know have iPhones, take Ubers, and vacation in Airbnbs because it makes sense – financially and otherwise. I’m guessing the technology adoption curve will hold true for ETFs as well and it’s only a matter of time before we see an influx of late majority, late adopters, and yes, even laggards in the ETF world.

“ETFs are fundamentally a technology. They are mechanisms to achieve a certain goal, like phones. Traditional mutual funds were rotary phones. ETFs are smartphones: They do the same thing but are in a better package.” – Dave Nadig, Managing Director of ETF.com in Barron’s