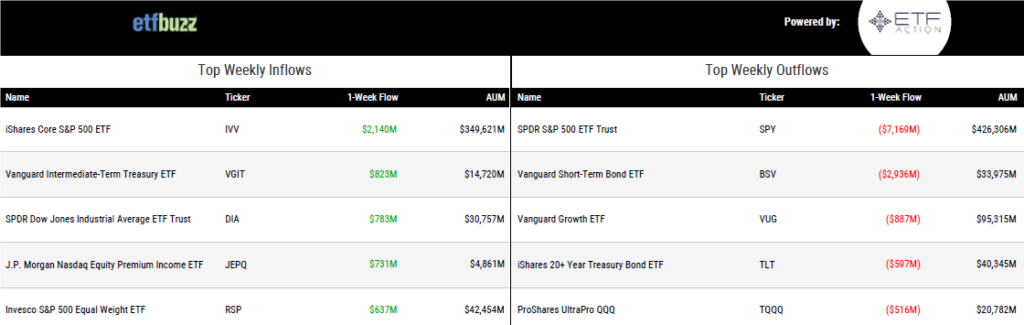

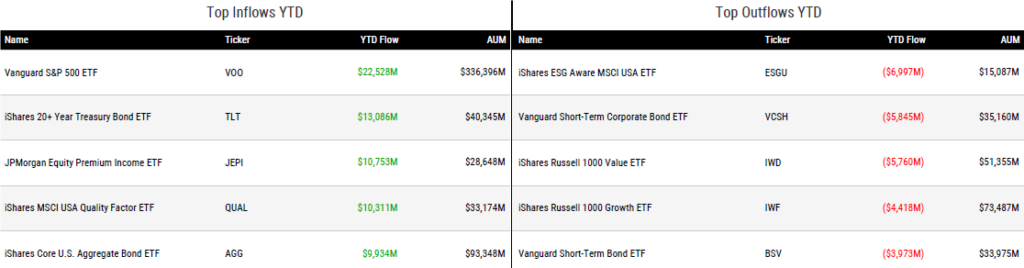

ETF Inflows & Outflows

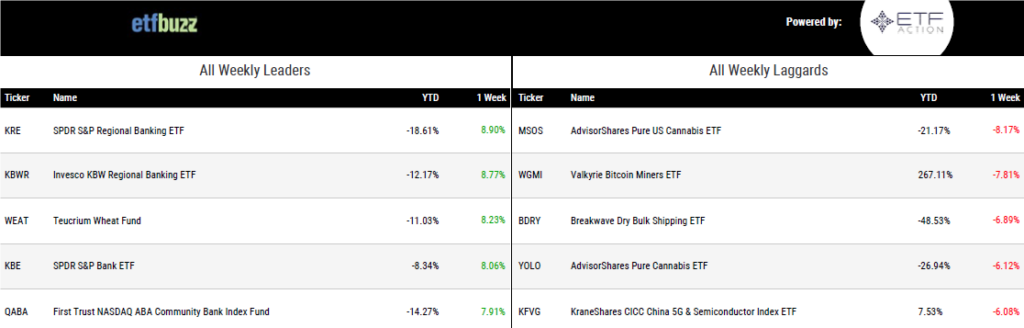

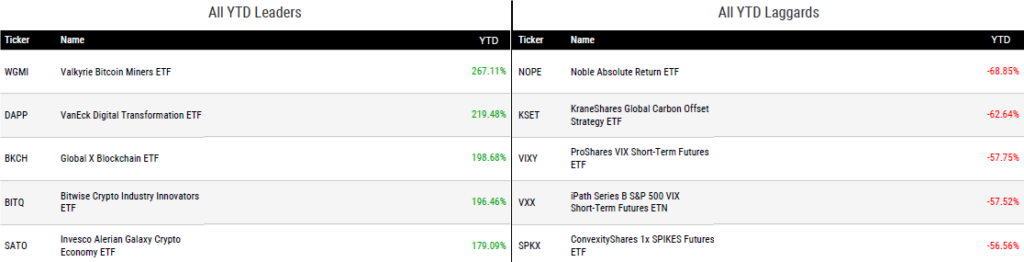

Performance Leaders & Laggards

Weekly ETF Reads

Young people far more likely to invest in ETFs than over 55s, says Invesco by Steve Randall

“Across all age groups, the study found a lack of understanding is the main barrier to ETF investing.”

First ETF with 100% protection against losses launches in US by Steve Johnson

“Innovator claims the ETF structure offers several advantages over annuities.”

TSLL Becomes First $1 Billion Single Stock ETF by Sumit Roy

“Tesla is a unique stock with a cultlike following.”

BlackRock offers a vote to retail investors in its biggest ETF by Brooke Masters

“Customers will not be able to cast specific votes on individual companies.”

Bitcoin ETF Hype Threatens Another Sell-The-News Fizzle by Vildana Hajric and Katie Greifeld

“It’s hard to overstate the amount of hype that’s surrounded the still-hypothetical spot fund.”

Start your engines: Deadlines to watch for in the bitcoin ETF race by Ben Strack

“They are now forced to make a decision one way or another.”

Despite BlackRock, Don’t Expect a Flood of Spot-Bitcoin ETFs Soon: Experts by Amitoj Singh

“The ETFs will not be approved until the Coinbase lawsuit is settled or squashed.”

The 2023 Intern’s Guide to ETFs by Phil Mackintosh

“ETFs are one of the most successful financial innovations of the last 30 years.”

ETF Tweet of the Week

As always, a little ETF education goes a long way. So, what is securities lending revenue you ask? Short sellers borrow shares of a stock hoping the price will go down and they can profit. A very simple example is a short seller who borrows shares trading at $40, immediately sells those shares for $40, and then buys them back when they fall to $30 in order to “pay off” the loan (thereby profiting $10/share). In order to borrow those shares, a short seller must pay a fee similar to the interest on any loan (the higher the demand to short particular shares, the higher the fee). Some investors might not realize that ETF issuers have the ability to lend out the securities held in an ETF to these short sellers. Note that these loans are fully backed by cash collateral. In return, the ETF receives the lending fee and also interest income from the collateral backing the loan. Together, this is referred to as “securities lending revenue”. Ultimately, it is up to the ETF issuer as to how much of this revenue to keep versus share with ETF holders. Here are the top 10 ETFs ranked by securities lending return…

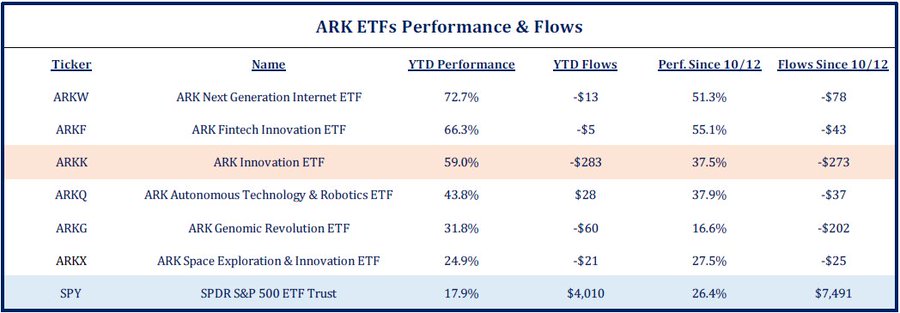

ETF Chart of the Week

Much has been made about the lack of flows into ARK’s ETF lineup, despite significant recent outperformance. My take on this is twofold: 1) Investors simply aren’t buying or believing in this year’s stock market rally in general. We can see that in equity ETF flows overall, which only total $150 billion – well off the scorching pace of the past several years. 2) ARK’s ETFs are still substantially below their all-time highs. For example, the ARK Innovation ETF (ARKK) is still down nearly 70% from its February 2021 high (though it is now back to outperforming the S&P 500 since its 2014 inception). Badly burned investors aren’t looking for an encore.

For her part, ARK’s Cathie Wood recently told the Wall Street Journal:

“We have been astonished at our asset retention since February of ‘21. It’s a very small number as a percentage of assets, which suggests that it’s far more likely to be people who are taking some profits than some exodus of people who have stayed in the fund through a prolonged down period.”

That appears true given that only $410 million has come out of the $16 billion ARK lineup (that’s 2.5% if you’re keeping track at home). This will be a story to watch the remainder of the year as a pickup in ARK inflows could indicate a “risk-on” market sentiment… or vice versa.