My favorite ETF reads over the past week, along with my ETF tweet and chart of the week!

How ETFs Are Passing the Banking Crisis Test to Provide Value by Matt Bartolini

“ETFs have long offered investors value as liquidity and price discovery tools during crises.”

What the World’s Most Boring Banking Crisis Means for Portfolios by Dave Nadig

“The most exposed ETF out there in the U.S. is the Vanguard FTSE Developed Markets ETF (VEA), and it had less than half a percent of Credit Suisse exposure before all this began.”

Largest ESG Fund Bleeds Cash Amid Political Backlash by Shubham Saharan

“Watered-down ESG isn’t working or a compelling story anymore to me.”

A Shift to Quality Is Not a Political Statement on ESG but the Market by Todd Rosenbluth

“Year-to-date, QUAL outperformed ESGU (6.5% vs. 4.5%).”

Jack Bogle Was Not Entirely Wrong About ETFs by John Rekenthaler

“Most ETF owners use their investments appropriately. That said, ETFs also qualify for a less prestigious honor: the home of the industry’s riskiest funds.”

ETF Tweet of the Week: Long-time followers know I’m fascinated by ETF innovation. Just when I think I’ve seen it all, something new comes along and captures my attention. This past week, Roundhill launched a first-of-its-kind product offering concentrated exposure to a specific sector. In this case, BIGB provides exposure to the six Global Systemically Important Banks – pretty timely! In order to achieve its concentrated exposure (it’s technically a “non-diversified” fund), the ETF holds a combination of total return swaps and the underlying individual stocks. In the coming weeks, Roundhill is planning on launching “BIG” ETFs covering technology, airlines, and defense.

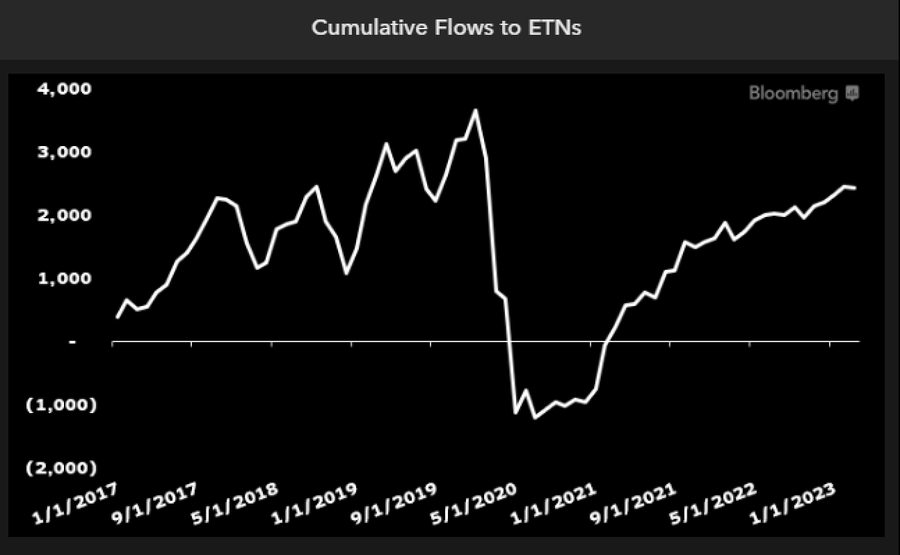

ETF Chart of the Week: Last week, I highlighted the credit risk involved with Exchange Traded Notes (ETNs). ETNs are simply unsecured debt securities. They don’t actually hold underlying stocks or bonds, but instead are a bank promise to pay out a particular return stream. That promise to pay obviously depends on a bank’s ability to do so. In my opinion, ETNs should be taken out behind the barn and shot. It’s not that the structure doesn’t have merits. ETNs can offer tax benefits, the ability to tightly track a benchmark, and more exotic exposure opportunities. The problem is the aforementioned credit risk and the fact that banks have a poor track record of properly supporting this structure. My experience is that retail investors simply don’t fully understand these potential issues.

Nevertheless, as Bloomberg’s Eric Balchunas points out, flows into ETNs have been increasing recently – primarily driven by products offering 3X leveraged exposure.