“You must pay taxes. But there’s no law that says you gotta leave a tip.” – Morgan Stanley

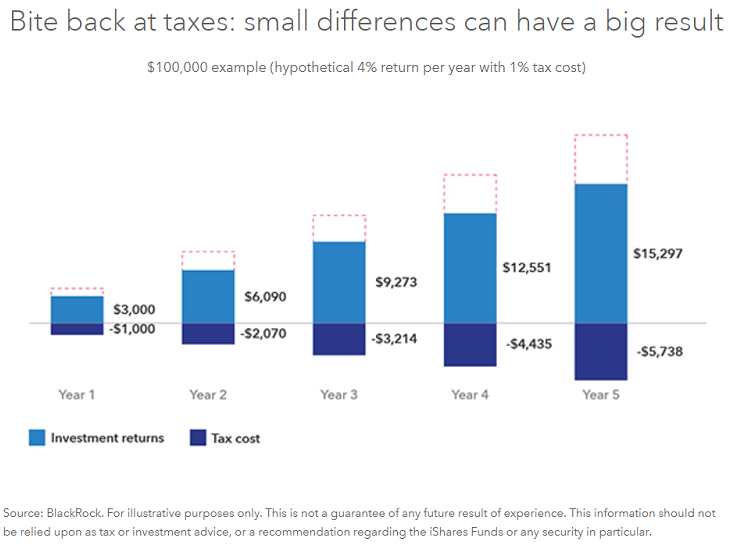

Unless you’re overly patriotic, highly altruistic, or have more money than you know what to do with, you likely agree paying less in taxes is better than paying more. There’s no reason to leave a tip for Uncle Sam each year. So, if there’s an easy way to legally reduce your tax bill, why not take advantage? Enter ETFs. While benefits such as lower costs, passive management, and transparency garner the headlines, the tax advantages of ETFs seem to fly under the radar. Compared to actively managed mutual funds, ETFs offer investors significantly more control over when they realize taxes, providing the opportunity for investment returns to compound within taxable accounts. If you don’t think taxes matter, consider the following basic illustration:

Source: iShares

Source: iShares

Source:

Source:

Why do ETFs have an advantage when it comes to taxes? Let’s walk through an example. Say you own shares of an actively managed mutual fund and another shareholder in the same fund wishes to sell their shares because they want to own bitcoin instead. In order to meet this redemption request, the manager of the mutual fund may need to sell shares of stocks held by the fund to raise the cash necessary to pay this shareholder. When the mutual fund manager sells shares of stocks owned by the fund for a gain, the mutual fund is required by law to distribute any net gains to all of the fund shareholders – including you! This is called a capital gain distribution and it typically occurs towards the end of each year. Here’s the kicker: you owe taxes on this distribution if the mutual fund is held in a taxable account. In 2018, the top capital gains tax rate is 20%, with high income earners paying an additional 3.8%.

So, let’s recap. Another mutual fund shareholder wants to take a flyer on bitcoin and because of that, you may be penalized with a taxable capital gain distribution. You didn’t sell your mutual fund shares at a gain. You didn’t receive an interest payment. You didn’t receive a dividend check. You didn’t do anything. But you may receive a tax bill, which hardly seems fair. What’s worse, these capital gain distributions are “phantom gains” in that the share price of the mutual fund is reduced by the amount of the capital gain distribution. Net-net, all you have gained is a tax bill.

Compare that with ETFs. If an ETF shareholder needs cash to purchase bitcoin, they simply sell their ETF shares to another investor on an exchange just like they would Apple or Facebook stock. There’s no impact to you. In other words, there’s no need for an ETF manager (provider) to sell shares of stocks held by the ETF to raise cash. It gets even better. In the event ETF shares are ultimately redeemed with the ETF provider, the unique ETF structure allows shares of underlying stocks to be delivered to Authorized Participants (APs) “in-kind”. This means shares of underlying stocks are exchanged for shares of the ETF – there’s no taxable event. A benefit of this process is that ETF providers can shed their lowest cost basis shares (which have the largest capital gains). For example, if an ETF owns a bunch of Amazon stock with a cost basis of $500 – and keep in mind, Amazon is trading at nearly $1,500 right now – when ETF shares are redeemed because there’s selling pressure in the market, the ETF provider can simply hand over that low-cost basis Amazon stock to an AP with no tax consequences. The benefit of this is that ETF providers can continually shed their lowest cost basis shares of stocks, providing a huge tax advantage compared to mutual funds. Interestingly, mutual funds will typically do exactly the opposite, shedding their highest cost basis holdings in an attempt to minimize their capital gain distributions.

Another, perhaps more significant, component of ETF tax efficiency is simply that most ETFs are passively managed. They track an index instead of paying a high-priced manager to pick individual stocks for the fund (which, historically, they haven’t been very good at). Passive management typically means lower turnover (less buying and selling) of the underlying stocks in the fund. That equates to fewer taxable events. The combination of the ETF structure and index-based strategies results in far fewer capital gain distributions for ETFs compared to active mutual funds. The below chart compares capital gain distributions for actively managed mutual funds and ETFs within the large-blend category:

Source: Morningstar

Source: Morningstar

Source:

Source:

It’s not just the large-blend category where there’s an advantage. According to iShares, the world’s largest ETF provider, 57% of all mutual funds paid out a capital gain distribution over the past five years compared to only 5% of iShares ETFs. That’s a staggering difference.

To be fair, mutual fund managers attempt to do everything they can to minimize capital gain distributions. Also, there are instances where ETFs may pay out distributions. If ETFs are forced to sell low cost basis holdings due to overall selling pressure in the market or if they reconstitute or rebalance holdings, that could generate capital gain distributions. Also, when you ultimately sell shares of either mutual funds or ETFs, you will have to pay taxes on any capital gains. But the structural advantage of ETFs is simply too much for active mutual funds to overcome. By not paying capital gain distributions, ETF investors can let the money they would have otherwise paid to Uncle Sam each year compound over time.

“Many people believe that where taxes are concerned, they are victims, held hostage by an inevitable process that allows them no input, no control. This passive approach becomes something of a self-fulfilling prophecy; where people believe that they lack control, they seldom try to assert control.” – Richard Carlson

It all boils down to control. With ETFs, you decide when to pay taxes. With mutual funds, you’re at the mercy of other shareholders and mutual fund manager decisions. If you own a particular mutual fund and another shareholder panic sells during a brief market downturn, you may be penalized with a tax bill (a number of mutual fund investors received a double whammy back in 2008 as their funds went down 30-40% AND they received taxable capital gain distributions). If a mutual fund shareholder sells their shares to buy bitcoin, you may get a tax bill. If a popular mutual fund manager decides to leave the company causing investors to sell their mutual fund shares – yup, you may get a tax bill. Also, think about the environment we’ve been in for 8+ years where stocks have risen substantially. Many mutual funds are sitting on large capital gains in underlying holdings. If they’re faced with significant redemptions, I shudder to think about what the capital gain distributions might look like.

Successful investing is about controlling the few factors you can – things like your behavior, investment costs, and taxes. ETFs simply provide investors greater control over taxes. While this benefit doesn’t necessarily receive the headlines it should, I believe it’s one of the key underlying drivers of the continued flow of investor dollars to ETFs and passive index funds and out of actively managed mutual funds.

Source: Morningstar

Source: Morningstar

Source:

Source:

Taxes might best be thought of in the same manner as fund fees – they’re costs that erode your returns over time. While low ETF fees receive the spotlight, the tax efficiency shouldn’t be overlooked – and both are a big problem for active mutual funds…

The more I think about it, the case for active high fee mutual fund complex being screwed is understated.

Average ETF fee advantage over mutual funds: 0.75%

Average ETF tax advantage over mutual funds: 0.80%Average mutual fund needs to be 1.5% better just to break even.

— Meb Faber (@MebFaber) March 26, 2018