Recently, I’ve seen lot of financial media and industry chatter regarding ETF costs – only not in the way you might expect. Instead of the usual talk about ETFs lowering the cost of investing or how ETF providers are ripping each other’s faces off in a race to see who can offer the cheapest ETF, the conversation is quickly shifting towards “cost isn’t everything”. Even Vanguard recently posted a blog titled “Is price everything for ETFs” where they concluded: “Low cost isn’t everything; it’s one factor among many other important factors”. Correct assessment but…Vanguard!!! It makes sense why fund companies are attempting to shift the focus away from fees – they are for-profit entities after all (well, except for Vanguard). “Feemaggedon” is grinding margins to the bone. The other media chatter I’ve seen seems to stem from the idea that advisors and investors may be focusing too much on cost, ignoring critical factors such as exposure and tracking error. That has me asking, “Are there really financial advisors selecting ETFs solely based on cost?!?”

Well, actually, I already know the answer to that. A recent ETF.com survey showed ETF investors (primarily advisors in this survey) cited expense ratio as the most important factor when selecting an ETF. As I discussed last week, it seems the DOL fiduciary rule is causing advisors to place a greater emphasis on cost. On the balance, I think this is a positive trend (more on that in moment). However, the DOL rule states brokers and advisors must “adhere to a best interest standard when making investment recommendations, charge no more than reasonable compensation for their services, and refrain from making misleading statements.” It does not say “simply select the lowest cost ETF”. I could make a highly convincing argument that selecting ETFs based purely on cost is actually a breach of an advisor’s fiduciary obligation.

This isn’t rocket science here. Any conversation surrounding which ETFs a client should own starts with a discussion around the types of investments, asset classes, and strategies that are appropriate for that client’s situation. Should they own U.S. stocks, international stocks, bonds, gold, REITs, etc.? How granular do you want to breakdown that exposure – large/mid/small cap, duration of bond holdings, credit quality, those sorts of things. How do you want to access that exposure? Do you want plain-vanilla market cap weighted strategies, “smart beta” strategies, traditional active management? It’s important to not work this process backwards. You don’t start with a list of ETFs, pick out the cheapest, and then try to figure out how to build a portfolio around them. Instead, asset allocation decisions should drive the decision-making process.

From there, the real homework begins – and, guess what? ETF cost is not at the top of the list. It starts with identifying ETFs offering exposure that best represents what you’re attempting to achieve in the portfolio. Exposure first – period. Next, it’s time to deep dive into factors such as how well an ETF tracks its index (or if active, look for high active share and how well the strategy aligns with your goals), liquidity/transaction costs (bid-ask, brokerage commissions), and for taxable accounts, the tax consequences of an ETF. All of these can impact your investment returns much more than cost. Cost actually falls down towards the end of the due diligence checklist.

Look, I am as guilty as anyone of beating the cost drum. I have my reasons. I believe “Exhibit A” is laid out in this piece I wrote last month. I’ll use this as “Exhibit B” (be sure to click through to Meb’s blog):

Mentioned this today…and still can’t get over all of these mutual funds charging > 1-2% for investing in the S&P 500…https://t.co/6thaPGV1aJ

— Meb Faber (@MebFaber) November 29, 2017

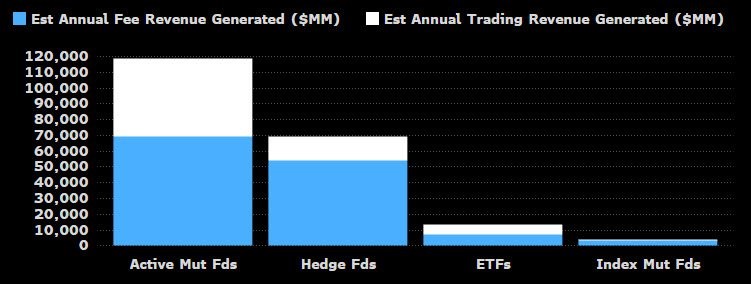

But, let’s not get the conversation surrounding ETF costs twisted. While costs shouldn’t drive the ETF selection process, that doesn’t mean it’s not important to emphasize. This year, mostly underperforming actively managed mutual funds and hedge funds are expected to generate far more fee and trading revenue than ETFs and index mutual funds.

Source: @EricBalchunas

Source: @EricBalchunas

Source:

Source:

That’s why I believe a focus on costs, whether driven by the DOL fiduciary rule or otherwise, is positive. Many of these funds are overcharging investors for closet indexing strategies or even worse, as Meb so colorfully pointed out. If you don’t think a focus on costs is still important and necessary, perhaps you’re part of the problem. Fund companies not adding meaningful value are attempting to paint advisors and investors who use low cost ETFs as somehow less sophisticated. These are the same fund companies who, again, typically underperform the market. For those fund companies attempting to add meaningful value (and they do exist – examples here & here), they should absolutely charge a reasonable fee reflecting the value provided.

Ultimately, money flows to where it’s best treated. However, even if you’re a fund company offering a real ability to treat money well, education and communication is key. Focus on educating clients on the value of your strategies, not throwing stones at ETFs you believe are intellectually inferior to what you’re doing. ETF.com’s Dave Nadig recently explained this beautifully. End clients aren’t as concerned with “low cost” per se. They want value for what they are paying for – just like anything else they purchase. If you can’t effectively communicate your value, maybe you don’t add any.

If you’re an advisor selecting funds purely based on costs, quite simply, you’re doing it wrong.